The Iran conflict continues to evolve rapidly. With the closure of the Straight of Hormuz (Associated Press 3/11) and attacks on both Iran and Qatar’s gas production facilities (NYTimes 3/18) international oil prices have soared. March Brent Crude oil prices have averaged over $98 a barrel – a 37% increase over February. Asian LNG markets have also risen sharply, though U.S. LNG prices have remained relatively stable (EIA, 3/10), largely because domestic supply and export capacity were already high.

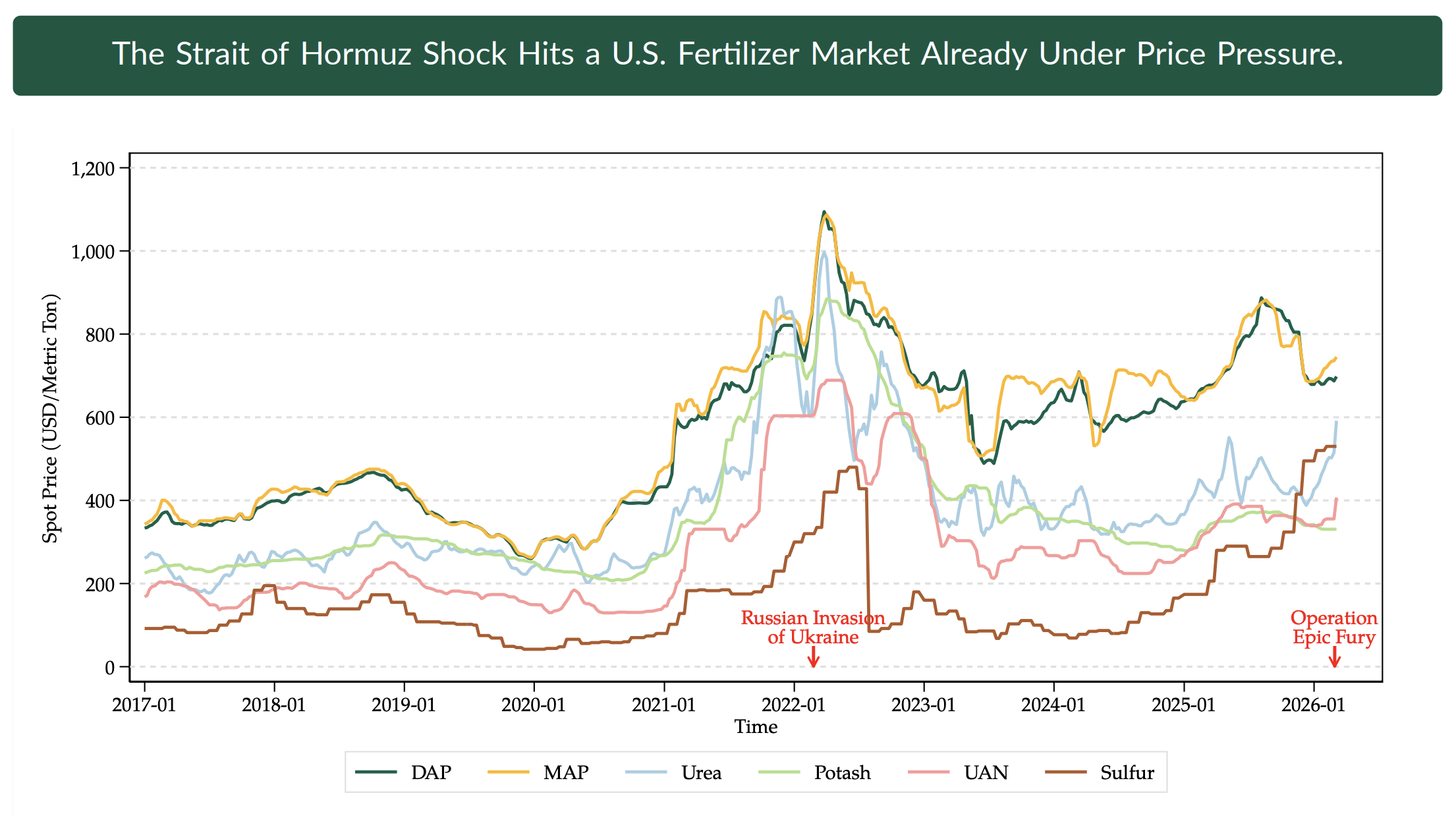

Agricultural production expenses had already been projected to be at a historic high for 2026 (ERS 2/5). Thus, the potential for further price increases has the agricultural community on alert. Oil and gas are directly and indirectly essential agriculture inputs. Directly, fuel is an important piece of a farm operations itself – accounting for about 3.5% of total input costs in Minnesota corn production, or roughly $30 per acre. Indirectly, fertilizer prices are closely linked to natural gas markets and often represent the largest single expense in row-crop systems, making up about 20% of total input costs in Minnesota corn production. We are currently seeing retail fertilizer prices increase. Urea is 11% higher than a month ago and Anhydrous is 8% more expensive relative to last month (DTN 3/25). The U.S. currently produces roughly 80% of nitrogen fertilizer domestically (ERS 2025), thus we don’t expect to see as big of a shock to fertilizer costs as Asian markets. Nonetheless, the increase in fertilizer expense for what was already the most expensive item on the balance sheet is expected to add further pressure to farm profitability.

In acknowledgement of both the current conflict and the uptick in fertilizer costs over the last decade, Senator Klobuchar, joined by Senators Thune and Marshall, introduced bipartisan legislation aimed at increasing fertilizer price transparency and lowering fertilizer costs creating mandatory price reporting.

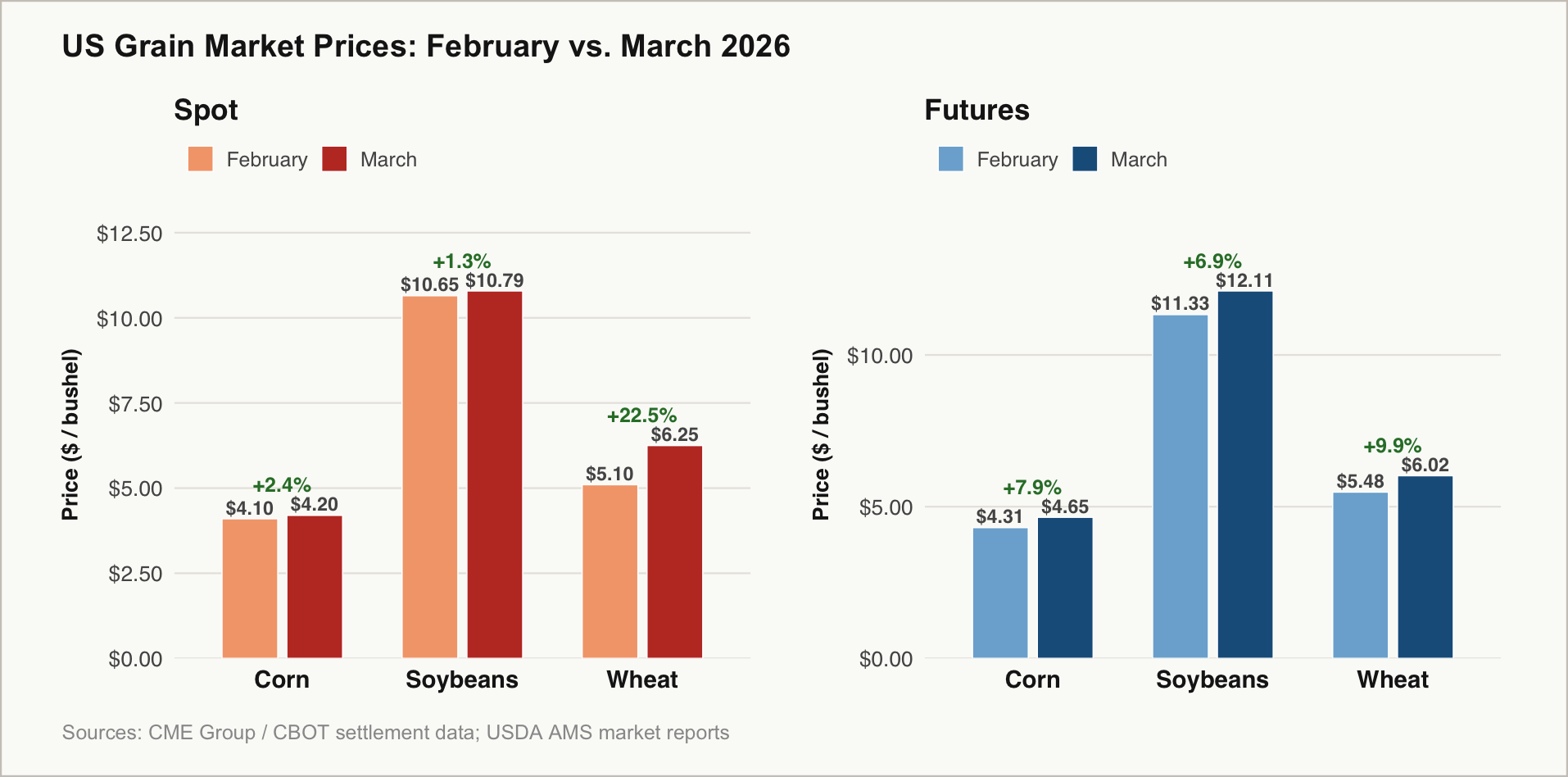

Finally, grain markets are beginning to respond, driven by expectations of higher production costs, tighter supply conditions, and possible trade disruptions. Over the coming weeks and months, prices will be influenced by transportation costs, shifts in global commodity supply, and rising agricultural production costs outside North America. March brought a broad upward move in grain markets, but the biggest immediate strength was in wheat, while corn and soybeans showed more of their strength in the futures market than in spot cash prices (Figure 2). That said, futures markets reflect speculations. Much will depend on how the conflict develops, whether supply disruptions persist, and how producers and traders adjust over the rest of the year.